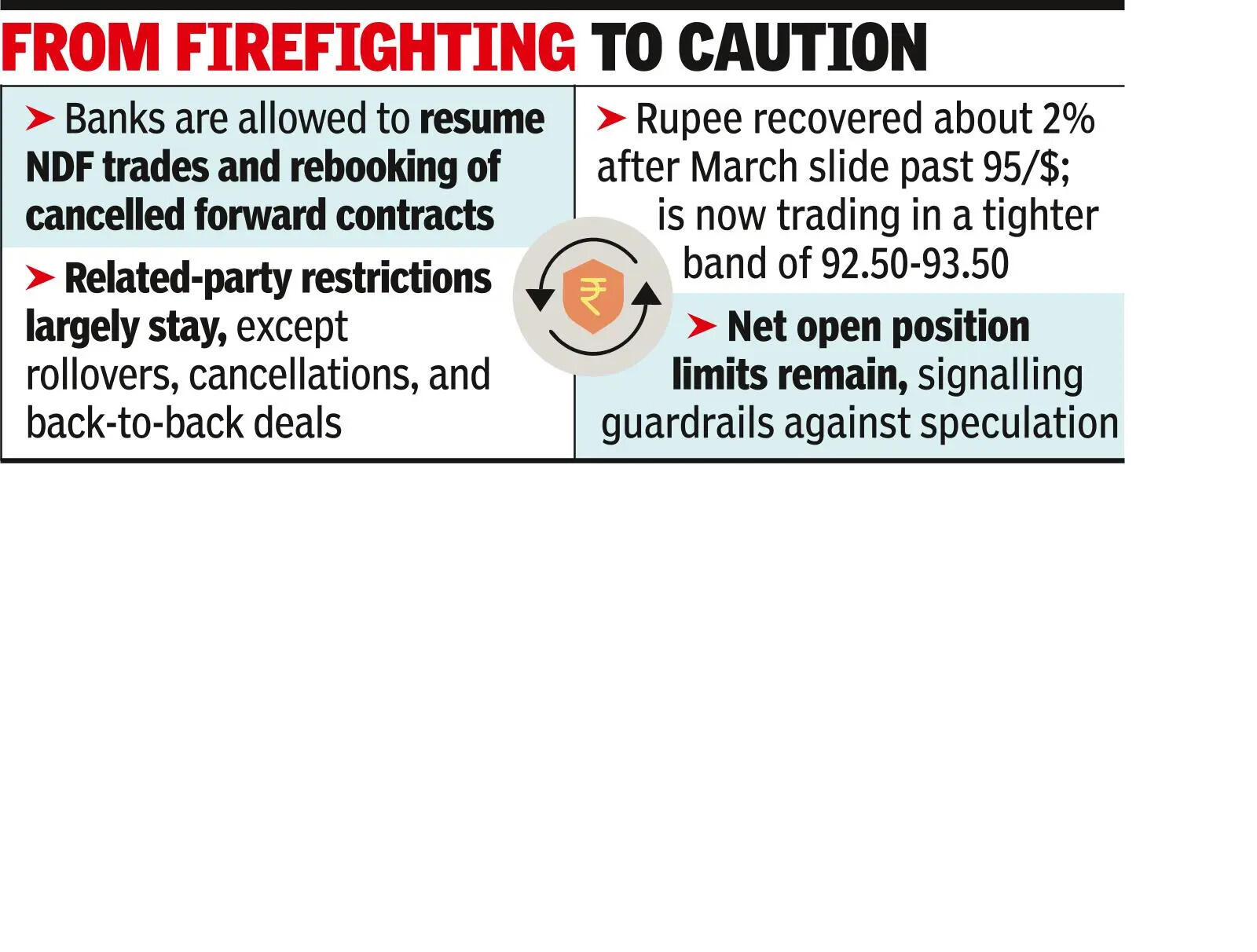

MUMBAI: RBI on Monday partially unwound emergency curbs on rupee derivatives, signalling a shift from firefighting to restoring normal market function after a spell of currency volatility.The central bank withdrew its April 1 directive, which had barred banks from offering non-deliverable forwards (NDFs)—offshore rupee derivatives settled in foreign currency—and prevented users from rebooking cancelled forward contracts. It also eased restrictions on dealings with non-related parties.Authorised dealers can now resume NDF trades and allow rebooking but must still avoid fresh rupee derivative contracts with related entities except for rollover or cancellation of existing trades and back-to-back transactions with unrelated non-resident users.The rollback follows a sequence of interventions triggered by the rupee’s slide past 95 to the dollar in late March. Initial measures sought to cap arbitrage and speculative positioning by limiting banks’ net open positions and tightening rules around derivatives. When those curbs proved insufficient with banks reportedly shifting exposures to corporates and affiliates, the RBI escalated restrictions on April 1, targeting related-party transactions and offshore instruments such as NDFs.

Those tighter controls achieved their immediate aim. The rupee rebounded about 2% and has since traded in a narrower band of 92.50–93.50. With volatility contained and positions largely unwound, the RBI appears to be recalibrating.The latest move suggests the central bank wants to restore hedging flexibility for genuine users while retaining guardrails against speculative or circular trades that amplify volatility. Limits on banks’ net open positions continue, and scrutiny of relatedparty transactions persists.The central bank’s rationale points to concerns over market conduct as much as currency stability. An unusual surge in high-volume related-party transactions had created artificial shortages and distorted price discovery. One of the rationales for the measures was that market makers are expected to meet client needs and not exploit liquidity access for proprietary gains. Earlier liberalisation had relaxed documentation requirements for hedging, but not to the extent of permitting unlimited round-tripping or profit-driven trades without underlying exposure.